Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on July 19, 2010

Registration No. 333-167611

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HUNTSMAN INTERNATIONAL LLC

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

2800 (Primary Standard Industrial Classification Code Number) |

87-0630358 (I.R.S. Employer IdentificationNumber) |

500 Huntsman Way

Salt Lake City, UT 84108

(801) 584-5700

(Address, Including Zip Code and Telephone Number, Including Area Code, of Registrants' Principal Executive Offices)

James R. Moore, Esq.

Executive Vice President, General Counsel and Secretary

Huntsman International LLC

500 Huntsman Way

Salt Lake City, UT 84108

(801) 584-5700

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copy to:

Nathan W. Jones, Esq.

Benjamin W. Bates, Esq.

Stoel Rives LLP

201 South Main Street, Suite 1100

Salt Lake City, UT 84111

(801) 328-3131

Exact Name of Additional Registrants*

|

Jurisdiction of Incorporation/Organization |

Primary Standard Industrial Classification Code Number |

I.R.S. Employer Identification Number |

||||||

|---|---|---|---|---|---|---|---|---|---|

Airstar Corporation |

Utah | 2800 | 87-0457111 | ||||||

Huntsman Advanced Materials Americas LLC |

Delaware | 2800 | 52-2215309 | ||||||

Huntsman Advanced Materials LLC |

Delaware | 2800 | 92-0194012 | ||||||

Huntsman Australia Inc. |

Utah | 2800 | 87-0510821 | ||||||

Huntsman Chemical Purchasing Corporation |

Utah | 2800 | 87-0568517 | ||||||

Huntsman Enterprises, Inc. |

Utah | 2800 | 87-0562447 | ||||||

Huntsman Ethyleneamines LLC |

Texas | 2800 | 87-0668124 | ||||||

Huntsman Fuels LLC |

Texas | 2800 | 91-2085706 | ||||||

Huntsman International Financial LLC |

Delaware | 2800 | 87-0632917 | ||||||

Huntsman International Fuels LLC |

Texas | 2800 | 91-2073796 | ||||||

Huntsman International Trading Corporation |

Delaware | 2800 | 87-0522263 | ||||||

Huntsman MA Investment Corporation |

Utah | 2800 | 87-0564509 | ||||||

Huntsman MA Services Corporation |

Utah | 2800 | 87-0661851 | ||||||

Huntsman Petrochemical LLC |

Delaware | 2800 | 58-1594518 | ||||||

Huntsman Petrochemical Purchasing Corporation |

Utah | 2800 | 87-0568520 | ||||||

Huntsman Procurement Corporation |

Utah | 2800 | 87-0644129 | ||||||

Huntsman Propylene Oxide LLC |

Texas | 2800 | 91-2073797 | ||||||

Huntsman Purchasing, Ltd. |

Utah | 2800 | 84-1370346 | ||||||

Polymer Materials Inc. |

Utah | 2800 | 87-0432897 | ||||||

Tioxide Americas Inc. |

Cayman Islands | 2800 | 98-0015568 | ||||||

Tioxide Group |

U.K. | 2800 | 98-0207605 | ||||||

Approximate date of commencement of proposed sale to the public: The Exchange will occur as soon as practicable after the effective date of this registration statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of each Class of Securities to be Registered |

Amount to be Registered |

Proposed Maximum Offering Price Per Note |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee |

||||

|---|---|---|---|---|---|---|---|---|

85/8% Senior Subordinated Notes due 2020 |

$350,000,000(1) | 100%(2)(3) | $350,000,000(1)(2) | $24,955(4) | ||||

Guarantees of 85/8% Senior Subordinated Notes due 2020 |

(5) | (5) | (5) | (5) | ||||

|

||||||||

The Registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any State in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such State.

SUBJECT TO COMPLETION—DATED JULY 19, 2010

PRELIMINARY PROSPECTUS

![]()

Huntsman International LLC

Offer to exchange $350,000,000 aggregate principal amount of

85/8% Senior Subordinated Notes due 2020

which have been registered under the Securities Act

for

$350,000,000 aggregate principal amount of

85/8% Senior Subordinated Notes due 2020

This exchange offer will expire at 12:01 a.m., New York City Time,

on , unless extended.

Terms of the exchange offer:

See the "Description of New Notes" section on page 180 for more information about the new notes to be issued in this exchange offer.

This investment involves risks. See the section entitled "Risk Factors" that begins on page 15 for a discussion of the risks that you should consider prior to tendering your old notes for exchange.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or the accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2010

Each broker-dealer that receives new notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the new notes it receives. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933, as amended. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of new notes received in exchange for old notes where such old notes were acquired by the broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 120 days after the consummation of the exchange offer, we will make this prospectus, as amended and supplemented, available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

We file annual, quarterly and certain other reports with the Securities and Exchange Commission jointly with our parent, Huntsman Corporation. Because Huntsman Corporation is not an obligor or guarantor under the notes and is not a registrant under the registration statement of which this prospectus is a part, certain notes to the financial statements included in this prospectus that relate solely to Huntsman Corporation have been omitted and are marked "[Reserved]".

i

The following summary highlights selected information from this prospectus and may not contain all the information that is important to you. This prospectus contains information regarding our business and detailed financial information. You should carefully read this entire document.

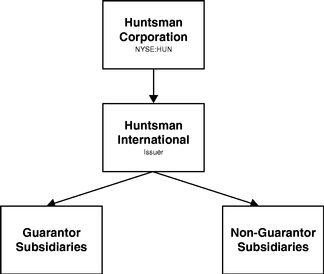

We are a wholly-owned subsidiary of Huntsman Corporation, which we refer to in this prospectus as our "parent." Unless the context otherwise requires: references in this prospectus to "we", "us", "our" or "our company" refer to Huntsman International LLC, together with its subsidiaries, and not to Huntsman Corporation and its other subsidiaries; references to "guarantors" or "guarantor subsidiaries" refer to our subsidiaries that have guaranteed our debt obligations, including the notes, consisting of substantially all of our domestic subsidiaries and certain of our foreign subsidiaries; "HPS" refers to Huntsman Polyurethanes Shanghai Ltd. (our consolidated splitting joint venture with Shanghai Chlor-Alkali Chemical Company, Ltd); and "SLIC" refers to Shanghai Liengheng Isocyanate Investment BV (our unconsolidated manufacturing joint venture with BASF AG and three Chinese chemical companies).

In this prospectus, we may use, without definition, the common names of competitors or other industry participants. We may also use the common names or abbreviations for certain chemicals or products. Many of these terms are defined in the Glossary of Chemical Terms that begins on 124 below.

Overview

We are a global manufacturer of differentiated organic chemical products and of inorganic chemical products. Jon M. Huntsman founded the predecessor to our company as a small polystyrene plastics packaging company. Since then, we have grown through a series of significant acquisitions and now own a portfolio of businesses. In 2005, our parent completed an initial public stock offering. Our products comprise a broad range of chemicals and formulations, which we market globally to a diversified group of consumer and industrial customers. Our products are used in a wide range of applications, including those in the adhesives, aerospace, automotive, construction products, durable and non-durable consumer products, electronics, medical, packaging, paints and coatings, power generation, refining, synthetic fiber, textile chemicals and dye industries. We are a leading global producer in many of our key product lines, including MDI, amines, surfactants, epoxy-based polymer formulations, textile chemicals, dyes, maleic anhydride and titanium dioxide. Our administrative, research and development and manufacturing operations are primarily conducted at the facilities listed below under "Business—Properties," which are located in 27 countries. As of December 31, 2009, we employed approximately 11,000 associates worldwide. We had revenues for the three months ended March 31, 2010 and 2009 of $2,094 million and $1,680 million, respectively, and for the years ended December 31, 2009, 2008 and 2007 of $7,665 million, $10,056 million and $9,496 million, respectively. Huntsman International LLC was organized in 1999 as a Delaware limited liability company. Our principal executive offices are located at 500 Huntsman Way, Salt Lake City, Utah 84108, and our telephone number at that location is (801) 584-5700.

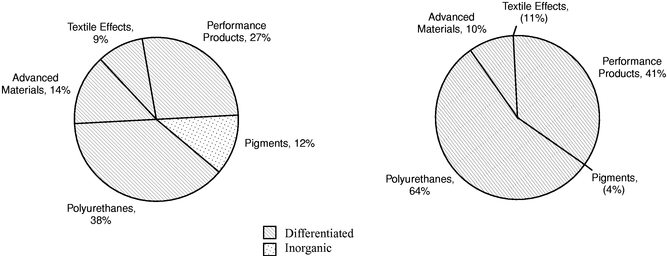

We operate in five segments: Polyurethanes, Performance Products, Advanced Materials, Textile Effects and Pigments. Our Polyurethanes, Performance Products, Advanced Materials and Textile Effects segments produce differentiated organic chemical products and our Pigments segment produces inorganic chemical products. We ceased operation of our Australian styrenics operations during the first quarter of 2010 and report the results of that business as discontinued operations. See "Note 19. Discontinued Operations" to our unaudited condensed consolidated financial statements included elsewhere in this prospectus and "Note 27. Discontinued Operations" to our audited consolidated financial statements included elsewhere in this prospectus.

1

The chart below generally illustrates our organizational structure:

Our Products

We produce differentiated organic chemical and inorganic chemical products. Our Polyurethanes, Advanced Materials, Textile Effects and Performance Products segments produce differentiated organic chemical products and our Pigments segment produces inorganic chemical products. Our former Polymers and Base Chemicals operations, which have been sold, produced commodity organic chemical products. For more information, see "Note 27. Discontinued Operations" to our audited consolidated financial statements included elsewhere in this prospectus and "Note 19. Discontinued Operations" to our unaudited condensed consolidated financial statements included elsewhere in this prospectus.

Growth in our differentiated products has been driven by the substitution of our products for other materials and by the level of global economic activity. Accordingly, the profitability of our differentiated products has been somewhat less influenced by the cyclicality that typically impacts the petrochemical

2

industry. Our Pigments business, while cyclical, is influenced largely by seasonal demand patterns in the coatings industry.

2009 Segment Revenues(1)

|

2009 Segment EBITDA from Continuing Operations(1) |

|

|---|---|---|

|

||

3

The following table identifies the key products, their principal end markets and applications and representative customers of each of our segments:

Segment

|

Products | End Markets and Applications |

Representative Customers |

|||

|---|---|---|---|---|---|---|

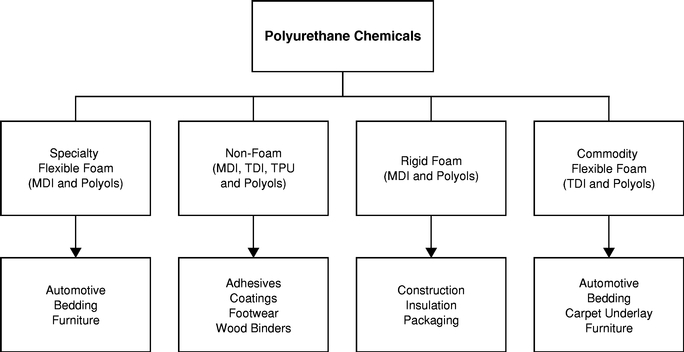

| Polyurethanes | MDI, PO, polyols, PG, TPU, aniline and MTBE | Refrigeration and appliance insulation, construction products, adhesives, automotive, footwear, furniture, cushioning, specialized engineering applications and fuel additives | BMW, Certainteed, Electrolux, Firestone, GE, Haier, Louisiana Pacific, Recticel, Weyerhauser | |||

Advanced Materials |

Basic liquid and solid epoxy resins; Specialty resin compounds; Cross-linking, matting and curing agents; epoxy, acrylic and polyure-thane-based formulations |

Adhesives, composites for aerospace, automotive, and wind power generation; construction and civil engineering; industrial coatings; electrical power transmission, consumer electronics |

ABB, Akzo, BASF, Boeing, Bosch, Cytec, Dow, Hexcel, Kansai, Omya, PPG, Samsung, Sanarrow, Schneider, Sherwin Williams, Siemens, Sika, Speed Fair, Syngenta, Toray |

|||

Textile Effects |

Textile chemicals and dyes |

Apparel, home and technical textiles |

Russell, Sara Lee, Sherwin Williams, Wellspun, Hanes Brands, Milliken |

|||

Performance Products |

Amines, surfactants, LAB, maleic anhydride, other performance chemicals, EG, olefins and technology licenses |

Detergents, personal care products, agrochemicals, lubricant and fuel additives, adhesives, paints and coatings, construction, marine and automotive products and PET fibers and resins |

Chevron, Henkel, The Sun Products Corporation, Monsanto, Procter & Gamble, Unilever, Lubrizol, Reichhold, Dow, L'Oreal, Afton |

|||

Pigments |

Titanium dioxide |

Paints and coatings, plastics, paper, printing inks, fibers and ceramics |

Akzo, Sigma Kalon, Clariant, Jotun, PolyOne |

4

Recent Developments

Fire Insurance Settlement

On May 14, 2010, we reached agreement with our insurance carriers to settle claims related to losses occurring as a result of the April 29, 2006 fire at our Port Arthur, Texas olefins facility, subsequently sold to Flint Hills Resources. Under the agreement, we received cash proceeds of $110 million in settlement of our claims, which had been the subject of ongoing arbitration with our carriers. We previously collected $365 million in insurance proceeds also related to the 2006 fire. We used these proceeds to retire secured debt.

Senior Subordinated Note Offering

On March 17, 2010 we completed the offering of the old notes. We used the net proceeds together with available cash on hand to redeem approximately €184 million (approximately $247 million as of March 31, 2010) senior subordinated notes due 2013 and approximately €59 million (approximately $79 million as of March 31, 2010) senior subordinated notes due 2015, and to pay fees, expenses and accrued interest in connection with the offering of the old notes and the subsequent redemption of outstanding notes. In connection with the redemption of these notes, we recorded a loss on early extinguishment of debt in the first quarter of 2010 of $9 million. In connection with these redemptions and the issuance of the old notes, we entered into $350 million notional amount of five-year euro/dollar cross-currency interest rate contracts. These swap transactions do not affect the interest payable to holders of notes under the terms of the notes.

Amendment to Senior Credit Facilities

On March 9, 2010, we entered into a Fifth Amendment to Credit Agreement (the "Amendment") with JPMorgan Chase Bank, N.A. and the other financial institutions party thereto, which amended certain terms of our existing senior credit facilities (the "Senior Credit Facilities"). Among other things, the Amendment (i) replaces Deutsche Bank AG New York Branch as administrative agent, collateral agent and U.K. security trustee with JPMorgan Chase Bank, N.A. as administrative agent and collateral agent and JPMorgan Chase Bank, N.A. or an affiliate thereof as U.K. security trustee, (ii) extends the stated maturity of the revolving facility to March 9, 2014, and (iii) limits the aggregate amount of the revolving commitments allowable under the revolving facility to an amount up to $300 million, including $225 million currently obtained from the lenders. The Amendment increases the applicable LIBOR margin range on our senior secured revolving facility (the "Revolving Facility") by 1.75% to 3.50% per annum and increased the unused commitment fee percentage to a range of 0.50% to 0.75%.

Accounting for our Accounts Receivable Securitization Program

On January 1, 2010, in connection with the adoption of ASU No. 2009-16, we have accounted for sales of accounts receivable under our accounts receivable securitization programs as secured borrowings. See "Note 2. Recently Issued Accounting Pronouncements" and "Note 7. Debt—Accounts Receivable Securitization" to our unaudited condensed consolidated financial statements included elsewhere in this prospectus.

5

Securities Offered |

$350,000,000 aggregate principal amount of new notes which have been registered under the Securities Act of 1933, as amended (the "Securities Act"). The terms of the new notes are substantially identical to the old notes, except that certain transfer restrictions, registration rights and liquidated damages provisions relating to the old notes do not apply to the registered new notes. | |

The Exchange Offer |

We are offering to issue registered new notes in exchange for like principal amount and like denomination of our old notes. We are offering to issue these registered new notes to satisfy our obligations under an exchange and registration rights agreement that we entered into with the initial purchasers of the old notes when we sold them in transactions that were exempt from the registration requirements of the Securities Act. You may tender your old notes for exchange by following the procedures described under the heading "The Exchange Offer." |

|

Tenders; Expiration Date; Withdrawal |

The exchange offer will expire at 12:01 a.m., New York City time, on , unless we extend it. If you decide to exchange your old notes for new notes, you must acknowledge, among other things, that you are acquiring the new notes in the ordinary course of your business, that you have no arrangement or understanding with any person to participate in a distribution of the new notes and that you are not an affiliate of our Company. You may withdraw any notes that you tender for exchange at any time prior to 12:01 a.m., New York City time, on the expiration date. If we decide for any reason not to accept any old notes you have tendered for exchange, those notes will be returned to you without cost promptly after the expiration or termination of the exchange offer. See "The Exchange Offer—Terms of the Exchange Offer" and "—Withdrawal Rights" for a more complete description of the tender and withdrawal provisions. |

|

Conditions to the Exchange Offer |

The exchange offer is subject to customary conditions and we may terminate or amend the exchange offer if any of these conditions occur prior to the expiration of the exchange offer. These conditions include any change in applicable law or legal interpretation or governmental or regulatory actions that would impair our ability to proceed with the exchange offer, any general suspension or general limitation relating to trading of securities on any national securities exchange or the over-the-counter market or a declaration of war or other hostilities involving the United States. We may waive any of these conditions in our sole discretion. |

6

Procedures for Tendering Old Notes |

A holder who wishes to tender old notes in the exchange offer must transmit to Wells Fargo Bank, N.A. (the "exchange agent") a completed and executed letter of transmittal or an agent's message, transmitted by a book-entry transfer facility, which letter of transmittal or agent's message must be received by the exchange agent prior to 12:01 a.m., New York City time, on the expiration date. In addition, the exchange agent must receive a timely confirmation of book-entry transfer of the old notes into the exchange agent's account at The Depository Trust Company, or DTC, under the procedures for book-entry transfers described in "The Exchange Offer—How to Tender Old Notes for Exchange." |

|

|

Old notes may be tendered by electronic transmission of acceptance through DTC's Automated Tender Offer Program, which we refer to as ATOP. Custodial entities that are participants in DTC must tender old notes through ATOP. A physical letter of transmittal need not accompany tenders effected through ATOP, although the electronic instructions sent to DTC and transmitted to the exchange agent must contain your acknowledgement of receipt of, and your agreement to be bound by, the letter of transmittal. Please carefully follow the instructions contained in this document on how to tender your securities. See "The Exchange Offer—DTC Book Entry Transfers." |

|

|

A holder who holds old notes through Euroclear Bank S.A./N.V. ("Euroclear") or Clearstream Banking, S.A. ("Clearstream") must comply with the procedures of Euroclear or Clearstream, as applicable, when tendering its old notes. |

|

Exchange Offer; Exchange and Registration Rights |

Under the exchange and registration rights agreement, we have agreed to use our reasonable best efforts to commence and consummate the exchange offer within 45 days after the date on which the registration statement of which this prospectus is a part is declared effective. In addition, we have agreed to file a "shelf registration statement" that would allow some or all of the old notes to be offered to the public if we are unable to complete the exchange offer or a change in applicable laws or legal interpretation occurs that would limit the intended effects or availability of the exchange offer. |

7

Penalty Interest |

If we fail to fulfill certain obligations under the exchange and registration rights agreement, including if the registration statement of which this prospectus is a part is not declared effective by the SEC on or before December 13, 2010 or if the exchange offer has not been completed within 45 business days after the effective date of such registration statement (a "registration default"), the annual interest rate on the notes will increase by 0.125% during the first 90-day period during which the registration default continues, and will increase by an additional 0.125% for each subsequent 90-day period during which the registration default continues, up to a maximum increase of 0.50% over the interest rate that would otherwise apply to the old notes. As soon as we cure a registration default, the interest rates on the new notes will revert to their original levels. |

|

U.S. Federal Tax Consequences |

Your exchange of old notes for new notes in the exchange offer will not result in any gain or loss to you for United States federal income tax purposes. See "Material United States Federal Income Tax Consequences." |

|

Use of Proceeds |

We will not receive any cash proceeds from the exchange offer. In consideration for issuing the new notes in the exchange offer as contemplated in this prospectus, we will receive in exchange old notes in like principal amount, which will be cancelled and as such will not result in any increase in our indebtedness. We will pay all expenses incident to the exchange offer. See "Use of Proceeds" for a discussion of the use of proceeds from the issuance of the old notes. |

|

Exchange Agent |

Wells Fargo Bank, N.A. |

|

Consequences of Failure to Exchange |

Old notes that are not tendered or that are tendered but not accepted will continue to be subject to the restrictions on transfer that are described in the legend on those notes. In general, you may offer or sell your old notes only if they are registered under, or offered or sold under an exemption from, the Securities Act and applicable state securities laws. We, however, will have no further obligation to register the old notes. If you do not participate in the exchange offer, the liquidity of your notes could be adversely affected. |

|

Consequences of Exchanging Your Old Notes |

Based on interpretations of the Securities and Exchange Commission, or SEC, set forth in certain no-action letters issued to third parties, we believe that you may offer for resale, resell or otherwise transfer the new notes that we issue in the exchange offer without complying with the registration and prospectus delivery requirements of the Securities Act if you: |

|

|

• acquire the new notes issued in the exchange offer in the ordinary course of your business; |

8

|

• are not participating, do not intend to participate, and have no arrangement or understanding with anyone to participate, in the distribution of the new notes issued to you in the exchange offer; and |

|

|

• are not an "affiliate" of our Company as defined in Rule 405 of the Securities Act. |

|

|

If any of these conditions are not satisfied and you transfer any new notes issued to you in the exchange offer without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We will not be responsible for, or indemnify you against, any liability you may incur. |

|

|

In connection with the exchange offer, you will be required to acknowledge that you are not engaged in, and do not intend to engage in, the distribution of the new notes. In addition, any broker-dealer that acquires new notes in the exchange offer for its own account in exchange for old notes which it acquired through market-making or other trading activities may be an "underwriter" within the meaning of the Securities Act and must acknowledge that it will deliver a prospectus when it resells or transfers any new notes. See "Plan of Distribution" for a description of the prospectus delivery obligations of broker-dealers in the exchange offer. |

9

The terms of the new notes and those of the old notes are identical in all material respects, except:

A brief description of the material terms of the new notes follows:

Issuer |

Huntsman International LLC. | |

Notes Offered |

$350 million in aggregate principal amount of 85/8% senior subordinated notes due 2020. |

|

Maturity |

March 15, 2020. |

|

Interest |

The new notes will bear interest at a rate of 85/8% per annum, payable semi-annually. |

|

Interest Payment Dates |

We will pay interest on the new notes each March 15 and September 15, beginning on September 15, 2010. |

|

Guarantees |

The new notes will be unconditionally guaranteed by substantially all of our domestic subsidiaries and certain of our foreign subsidiaries. If we cannot make payments on the notes when they are due, then our subsidiary guarantors are required to make payments on our behalf. See "Description of New Notes—Brief Description of the Notes and the Guarantees—The Guarantees." |

|

Ranking |

The new notes will be: |

|

|

• our general unsecured senior subordinated obligations; |

|

|

• subordinated in right of payment to all our existing and future senior indebtedness and structurally subordinated to all liabilities (including trade payables) of our subsidiaries which are not guarantors (except with respect to indebtedness owed to us or other guarantors); |

|

|

• equal in right of payment to all our existing and future senior subordinated indebtedness; and |

|

|

• unconditionally guaranteed by the guarantors on a senior subordinated basis. |

|

|

Since the new notes are unsecured, in the event of a bankruptcy or insolvency, our secured creditors will have a prior secured claim to any collateral securing the debt owed to them. |

|

|

The guarantees will be: |

|

|

• the general unsecured senior subordinated obligations of the guarantors; |

10

|

• subordinated in right of payment to all existing and future senior indebtedness of the guarantors; and |

|

|

• equal in right of payment to all existing and future subordinated indebtedness of the guarantors. |

|

|

Since the guarantees are unsecured obligations of each guarantor, in the event of a bankruptcy or insolvency, such guarantor's secured creditors will have a prior secured claim to any collateral securing the debt owed to them. |

|

|

As of March 31, 2010, we and the guarantors had approximately $2.4 billion of outstanding senior indebtedness (excluding intercompany indebtedness), of which approximately $2.0 billion was secured. We and the guarantors had approximately $1.7 billion of other indebtedness (excluding intercompany indebtedness, except for the $425 million note payable to our parent) outstanding (after giving effect to the issuance of the notes and the application of the estimated net proceeds of the offering of the notes) that rank equally in right of payment with the notes. In addition, our subsidiaries which are not guarantors had approximately $507 million of indebtedness (excluding intercompany indebtedness) outstanding on March 31, 2010. See "Note 22. Condensed Consolidating Financial Information (Unaudited)" to the unaudited condensed consolidated financial statements included elsewhere in this prospectus for certain financial information about our non-guarantor subsidiaries as of March 31, 2010. |

|

Asset Sale Proceeds |

We may have to use the net proceeds from asset sales to offer to repurchase the notes under certain circumstances at their face amount, plus accrued and unpaid interest, if any, to the date of repurchase. See "Description of New Notes—Certain Covenants—Limitation on Asset Sales." |

|

Certain Covenants |

The indenture governing the notes contains covenants that, among other things, limit our ability and the ability of certain of our subsidiaries to: |

|

|

• incur additional indebtedness; |

|

|

• pay dividends or distributions on or redeem, repurchase or acquire our capital stock; |

|

|

• make certain investments; |

|

|

• create liens; |

|

|

• engage in transactions with affiliates; |

|

|

• merge or consolidate; and |

|

|

• transfer or sell assets. |

|

|

These covenants are subject to a number of important exceptions and qualifications, which are described in "Description of New Notes—Certain Covenants." |

11

|

Certain of these covenants will terminate if the notes attain an investment grade rating. |

|

Risk Factors |

You should carefully consider all the information set forth in this prospectus and, in particular, should evaluate the specific risk factors set forth under "Risk Factors," beginning on page 15, before participating in this exchange offer. |

For additional information regarding the new notes, see "Description of New Notes."

FAILURE TO EXCHANGE YOUR OLD NOTES

The old notes which you do not tender or we do not accept will, following the exchange offer, continue to be restricted securities. Therefore, you may only transfer or resell them in a transaction registered under or exempt from the Securities Act and all applicable state securities laws. We will issue the new notes in exchange for the old notes under the exchange offer only following the satisfaction of the procedures and conditions described under the caption "The Exchange Offer."

Because we anticipate that most holders of the old notes will elect to exchange their old notes, we expect that the liquidity of the markets, if any, for any old notes remaining after the completion of the exchange offer will be substantially limited. Any old notes tendered and exchanged in the exchange offer will reduce the aggregate principal amount outstanding of the old notes.

As of March 31, 2010, we had $4.3 billion in debt outstanding other than the old notes.

The indenture governing the notes limits our ability to incur additional debt. Consequently, we would be required to obtain an amendment of the indenture before we incurred any additional debt, other than the types of debt specifically identified in the indenture as permitted.

12

SUMMARY HISTORICAL FINANCIAL DATA

The summary historical financial data set forth below presents our historical financial data as of and for the dates and periods indicated. You should review this summary historical financial data in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operation" and our audited consolidated financial statements, unaudited condensed consolidated financial statements and accompanying notes and other financial information included elsewhere in this prospectus.

(in millions)

| |

Summary Historical Financial Data | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Three Months Ended March 31, |

Year Ended December 31, | ||||||||||||||||||||

| |

2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

Statements of Operations Data: |

||||||||||||||||||||||

Revenues |

$ | 2,094 | $ | 1,680 | $ | 7,665 | $ | 10,056 | $ | 9,496 | $ | 8,536 | $ | 8,232 | ||||||||

Gross profit |

286 | 154 | 1,095 | 1,297 | 1,551 | 1,431 | 1,432 | |||||||||||||||

Restructuring, impairment and plant closing costs |

3 | 14 | 88 | 31 | 29 | 8 | 59 | |||||||||||||||

Operating income (loss) |

39 | (77 | ) | 41 | 215 | 569 | 672 | 640 | ||||||||||||||

(Loss) income from continuing operations |

(13 | ) | (281 | ) | (399 | ) | (59 | ) | 232 | 272 | 115 | |||||||||||

(Loss) income from discontinued operations, net of tax(a) |

(13 | ) | (4 | ) | (19 | ) | 84 | (246 | ) | (122 | ) | 54 | ||||||||||

Extraordinary gain (loss) on the acquisition of a business, net of tax of nil(b) |

— | — | 6 | 14 | (7 | ) | 56 | — | ||||||||||||||

Cumulative effect of changes in accounting principle, net of tax(c) |

— | — | — | — | — | — | (28 | ) | ||||||||||||||

Net (loss) income |

(26 | ) | (285 | ) | (412 | ) | 39 | (21 | ) | 237 | 141 | |||||||||||

Net (loss) income attributable to Huntsman International LLC |

(26 | ) | (281 | ) | (410 | ) | 38 | (12 | ) | 234 | 139 | |||||||||||

Other Data: |

||||||||||||||||||||||

Depreciation and amortization |

$ | 92 | $ | 120 | $ | 420 | $ | 374 | $ | 391 | $ | 439 | $ | 475 | ||||||||

Capital expenditures |

37 | 61 | 189 | 418 | 665 | 550 | 339 | |||||||||||||||

Balance Sheet Data (at period end): |

||||||||||||||||||||||

Total assets |

$ | 7,749 | $ | 7,216 | $ | 7,693 | $ | 7,424 | $ | 8,095 | $ | 8,196 | $ | 8,633 | ||||||||

Total debt |

4,605 | 4,493 | 4,531 | 4,076 | 3,574 | 3,649 | 4,458 | |||||||||||||||

Total liabilities |

6,961 | 6,683 | 6,846 | 6,505 | 6,179 | 6,633 | 7,281 | |||||||||||||||

13

14

You should carefully consider the risks and uncertainties below and the other information contained in this prospectus before you decide whether to exchange your old notes for new notes. The risks and uncertainties described below are not the only risks we may face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business operations. Any of the following risks could materially and adversely affect our business, results of operations and financial condition. In this section of the prospectus, references to the notes mean the new notes.

Risks Related to Our Business

Our industry is affected by global economic factors including risks associated with declining economic conditions.

Our financial results are substantially dependent upon overall economic conditions in the United States, the European Union and Asia. Declining economic conditions in all or any of these locations—or negative perceptions about economic conditions—could result in a substantial decrease in demand for our products and could adversely affect our business. Indeed, as a result of the current economic downturn, we have experienced decreased demand for many of our products.

Uncertain economic conditions and market instability make it difficult for us, our customers and our suppliers to forecast demand trends. Renewed declines in demand would place additional pressure on our results of operations. The timing and extent of any changes to currently prevailing market conditions is uncertain and supply and demand may be unbalanced at any time. As a consequence, at present, we are unable to accurately predict future economic conditions or the effect of such conditions on our financial condition or results of operations, and we can give no assurances as to the timing, extent or duration of the current or future economic cycles impacting the chemical industry.

Significant price volatility or interruptions in supply of our raw materials may result in increased costs that we may be unable to pass on to our customers, which could reduce our profitability.

The prices of the raw materials that we purchase from third parties are cyclical and volatile. We purchase a substantial portion of these raw materials from third party suppliers, and, following the dispositions of our polymers and base chemicals businesses in 2007 and 2006, respectively, our purchases of certain products from third party suppliers have significantly increased. The cost of these raw materials represents a substantial portion of our operating expenses. The prices for a number of these raw materials generally follow price trends of, and vary with market conditions for, crude oil and natural gas feedstocks, which are highly volatile and cyclical.

The feedstocks and other raw materials we consume are generally commodity products that are readily available at market prices. We frequently enter into supply agreements with particular suppliers, but disruptions of existing supply arrangements could substantially impact our profitability. If certain of our suppliers are unable to meet their obligations under present supply agreements, we may be forced to pay higher prices to obtain the necessary raw materials from other sources and we may not be able to increase prices for our finished products to recoup the higher raw materials costs. In addition, if any of the raw materials that we use become unavailable within the geographic area from which they are now sourced, then we may not be able to obtain suitable or cost effective substitutes. Any interruption in the supply of raw materials could increase our costs or decrease our revenues, which could reduce our cash flow.

Our supply agreements typically provide for market-based pricing and provide us only limited protection against price volatility. While we attempt to match cost increases with corresponding product price increases, we are not always able to raise product prices immediately or at all. Timing differences

15

between raw material prices, which may change daily, and contract product prices, which in many cases are negotiated only monthly or less often, have had and may continue to have a negative effect on our cash flow. Any cost increase that we are not able to pass on to our customers could have a material adverse effect on our business, results of operations, financial condition and liquidity.

Financial difficulties and related problems at our customers, vendors, suppliers and other business partners could have a material adverse effect on our business.

The recent economic downturn has caused financial problems at some customers, vendors, suppliers and business partners. We rely on numerous vendors and suppliers and collaborations with other industry participants to provide us with chemicals, feedstocks and other raw materials, along with energy sources and, in certain cases, facilities, that we need to operate our business. If the economic downturn were to continue or worsen, some of these companies may be forced to reduce their output, shut down their operations or file for bankruptcy protection. If this were to occur, it could materially adversely affect their ability to provide us with the raw materials, energy sources or facilities that we need, which could disrupt our operations, including the production of certain of our products. In addition, it could be difficult to find replacements for certain of our business partners without incurring significant delays or cost increases.

In addition, if the economic downturn were to continue or worsen, some of our customers may experience financial difficulties, including bankruptcies, restructurings and liquidations, which could affect our business by reducing sales, increasing our risk in extending trade credit to customers and reducing our profitability. A significant adverse change in a customer relationship or in a customer's financial position could cause us to limit or discontinue business with that customer, require us to assume more credit risk relating to that customer's receivables or limit our ability to collect accounts receivable from that customer, all of which could have a material adverse effect on our business, results of operations, financial condition and liquidity.

Our available cash and access to additional capital may be limited by our significant leverage, which could restrict our ability to grow our businesses.

We have a significant amount of indebtedness outstanding. As of March 31, 2010, we had total consolidated outstanding indebtedness of approximately $4.6 billion (including the current portion of long-term debt) and a debt to total capitalization ratio of approximately 85%. Our outstanding debt could have important consequences for our businesses, including the following:

We require substantial capital to finance our operations and continued growth, and we may incur substantial additional debt from time to time for a variety of purposes, including acquiring additional businesses. However, our existing debt instruments contain restrictive covenants. Among other things, these covenants limit or prohibit our ability to incur more debt; make prepayments of other debt; pay

16

dividends, redeem stock or make other distributions; issue capital stock; make investments; create liens; enter into transactions with affiliates; enter into sale and leaseback transactions; merge or consolidate; and transfer or sell assets.

Our debt instruments also require us to comply with certain financial covenants under certain circumstances. For example, our Senior Credit Facilities are subject to a single financial covenant (the "Leverage Covenant") which applies only to the Revolving Facility. The Leverage Covenant is applicable only if borrowings, letters of credit or guarantees are outstanding under the Revolving Facility (cash collateralized letters of credit or guarantees are not deemed outstanding). Following the termination of a previous covenant waiver from the "revolver" lenders under the Senior Credit Facilities (the "2009 Waiver"), the Leverage Covenant is a net senior secured leverage covenant, with a maximum ratio of senior secured debt to EBITDA (as defined in the applicable agreement) of no more than 3.75 to 1. However, if we violate this covenant, it could lead to an event of default under the Senior Credit Facilities, which could require us to pay off the balance of the Senior Credit Facilities in full and result in a loss of such facilities. Given the current credit environment, it may not be possible for us to replace the Senior Credit Facilities with a substitute facility on terms acceptable to us, or at all.

We also must comply with certain financial covenants under our $250 million U.S. accounts receivable securitization program ("U.S. A/R Program") and our €225 million (approximately $302 million at March 31, 2010) European accounts receivable securitization program ("EU A/R Program," and, collectively with the U.S. A/R Program, our "A/R Program" or "A/R Programs"). Failure to meet such covenants could lead to an event of default and could require us to cease use of such facilities, thus prohibiting us from borrowing against our receivables. A default under our A/R Program would also constitute an event of default under our Senior Credit Facilities, which could require us to pay off the balance of the Senior Credit Facilities in full and result in a loss of such facilities. In summary, if debt under one or more of our facilities is accelerated, cross-default provisions in our debt instruments would likely be triggered, which would likely have a material adverse impact on our financial condition.

Also, if we undergo a change of control (which, as defined in our indentures, generally excludes transactions approved by our board of managers), our debt instruments may require us to make an offer to purchase certain of our notes. Under these circumstances, we may also be required to repay indebtedness under our Senior Credit Facilities prior to our notes. In this event, we may not have the financial resources necessary to purchase such notes, which would result in an event of default under the indentures governing such notes.

As of March 31, 2010, the current portion of our long term debt and notes payable to affiliates totaled approximately $416 million. As of March 31, 2010, we had combined outstanding variable rate borrowings of approximately $2.9 billion. Assuming a 1% increase in interest rates, without giving effect to any interest rate hedges, our annual interest rate expense would increase by approximately $29 million. If we are unable to generate sufficient cash flow or are otherwise unable to obtain the funds required to meet payments of principal and interest on our indebtedness, or if we otherwise fail to comply with the various covenants in the instruments governing our indebtedness, we could be in default under the terms of those instruments. In the event of a default, a holder of the indebtedness could elect to declare all the funds borrowed under those instruments to be due and payable together with accrued and unpaid interest, the creditors under our Senior Credit Facilities could elect to terminate their commitments thereunder and we or one or more of our subsidiaries could be forced into bankruptcy or liquidation. Any of the foregoing consequences could have a material adverse effect on our business, results of operations and financial condition.

17

We may not be able to obtain funding because of the deterioration of the credit and capital markets. This may hinder or prevent us from meeting our future capital needs and from refinancing our existing indebtedness when it comes due.

Global financial markets and economic conditions continue to be volatile, which has resulted in substantial deterioration in the credit and capital markets. These conditions, along with significant write-offs in the financial services sector and the re-pricing of credit risk, may make it difficult to obtain funding for our ongoing capital needs.

In particular, the cost of raising money in the debt and equity capital markets has increased substantially while the availability of funds from those markets generally has diminished. Also, as a result of concerns about the stability of financial markets generally and the solvency of counterparties specifically, the cost of obtaining money from the credit markets generally has increased as many lenders and institutional investors have increased interest rates, enacted tighter lending standards, refused to refinance existing debt at maturity on terms that are similar to existing debt, and reduced, or in some cases ceased, to provide funding to borrowers.

Due to these factors, we cannot be certain that additional funding for our capital needs from credit and capital markets will be available if needed and, to the extent required, on acceptable terms. In addition, we may be unable to refinance our existing indebtedness when it comes due on terms that are acceptable to us or at all. If we cannot meet our capital needs or refinance our existing indebtedness, it could have a material adverse effect on our financial position and results of operations.

A downgrade in the ratings of the securities of our company or our subsidiaries could result in increased interest and other financial expenses related to future borrowings of our company or our subsidiaries and could restrict our access to additional capital or trade credit.

Standard and Poor's Ratings Services and Moody's Investors Service maintain credit ratings for our company. Each of these ratings is currently below investment grade. Any decision by these or other ratings agencies to downgrade such ratings in the future could result in increased interest and other financial expenses relating to our future borrowings and could restrict our ability to obtain additional financing on satisfactory terms. In addition, any downgrade could restrict our access to, and negatively impact the terms of, trade credit extended by our suppliers of raw materials.

The industries in which we compete are highly competitive, and we may not be able to compete effectively with our competitors that have greater financial resources, which could have a material adverse effect on our business, results of operations and financial condition.

The industries in which we operate are highly competitive. Among our competitors are some of the world's largest chemical companies and major integrated petroleum companies that have their own raw material resources. Changes in the competitive landscape could make it difficult for us to retain our leadership position in various products and markets throughout the world. In addition, some of the companies with whom we compete may be able to produce products more economically than we can. Furthermore, some of our competitors have greater financial resources, which may enable them to invest significant capital into their businesses, including expenditures for research and development. While we are engaged in a range of research and development programs to develop new products and processes, to improve and refine existing products and processes, and to develop new applications for existing products, the failure to develop new products, processes or applications could make us less competitive. Moreover, if any of our current or future competitors develops proprietary technology that enables them to produce products at a significantly lower cost, our technology could be rendered uneconomical or obsolete.

In addition, certain of our businesses use technology that is widely available. Accordingly, barriers to entry, apart from capital availability, may be low in certain product segments of our business, and

18

the entrance of new competitors into the industry may reduce our ability to capture improving profit margins in circumstances where capacity utilization in the industry is increasing. Further, petroleum-rich countries have become more significant participants in the petrochemical industry and may expand this role significantly in the future. Increased competition in any of our businesses could compel us to reduce the prices of our products, which could result in reduced profit margins and loss of market share and have a material adverse effect on our business, results of operations, financial condition and liquidity.

Future acquisitions, partnerships and joint ventures may require significant resources and/or result in unanticipated adverse consequences that could have a material adverse effect on our business, results of operations and/or financial condition.

In the future we may seek to grow by making acquisitions or entering into partnerships and joint ventures. Any future acquisition, partnership or joint venture may require that we make a significant cash investment, issue stock or incur substantial debt. In addition, acquisitions, partnerships or investments may require significant managerial attention, which may be diverted from our other operations. These capital, equity and managerial commitments may impair the operation of our businesses. Any future acquisitions of businesses or facilities could entail a number of additional risks, including:

We have incurred indebtedness to finance past acquisitions. We may finance future acquisitions with additional indebtedness. We could face financial risks associated with incurring additional indebtedness, such as reducing our liquidity and access to financial markets and increasing the amount of cash flow required to service indebtedness, which could have a material adverse effect on our business, results of operations and financial condition.

Our results of operations may be adversely affected by international business risks, including fluctuations in currency exchange rates, legal restrictions and taxes.

We conduct a majority of our business operations outside the U.S., and these operations are subject to risks normally associated with international operations. These risks include the need to convert currencies that may be received for our products into currencies in which we purchase raw materials or pay for services, which could result in a gain or loss depending on fluctuations in exchange rates. In addition, we translate our local currency financial results into U.S. dollars based on average exchange rates prevailing during the reporting period or the exchange rate at the end of that period. During times of a strengthening U.S. dollar, our reported international sales and earnings may be reduced because the local currency may translate into fewer U.S. dollars. Because we currently have significant operations located outside the U.S., we are exposed to fluctuations in global currency rates which may result in gains or losses on our financial statements.

Other risks of international operations include trade barriers, tariffs, exchange controls, national and regional labor strikes, social and political risks, general economic risks and required compliance with a variety of U.S. and foreign laws, including tax laws. Furthermore, in foreign jurisdictions where process of law may vary from country to country, we may experience difficulty in enforcing agreements. In jurisdictions where bankruptcy laws and practices may vary, we may experience difficulty collecting foreign receivables through foreign legal systems. The occurrence of these risks, among others, could

19

disrupt the businesses of our international subsidiaries, which could significantly affect their ability to make distributions to us.

We operate in a significant number of jurisdictions, which contributes to the volatility of our effective tax rate. Changes in tax laws or the interpretation of tax laws in the jurisdictions in which we operate may affect our effective tax rate. In addition, generally accepted accounting principles in the U.S. have required us to place valuation allowances against our net operating losses and other deferred tax assets in a significant number of tax jurisdictions. These valuation allowances result from a cumulative history of pre-tax operating losses in specific tax jurisdictions. Valuation allowances have resulted in material fluctuations in our effective tax rate. Economic conditions may dictate the continued imposition of the current valuation allowances and potentially the establishment of new valuation allowances. While significant valuation allowances remain, our effective tax rate will likely continue to experience significant fluctuations.

The current administration has announced several proposals to reform U.S. tax laws, including a proposal to further limit foreign tax credits and a proposal to defer tax deductions allocable to non-U.S. earnings until earnings are repatriated. It is unclear whether these proposed changes will be enacted, or, if enacted, what the scope of the reforms will be. Depending on their content, such reforms, if enacted, could have a material adverse effect on our operating results and financial condition.

Demand for many of our products is cyclical, and we may experience depressed market conditions for such products.

Historically, the markets for many of our products have experienced alternating periods of tight supply, causing prices and profit margins to increase, followed by periods of capacity additions, resulting in oversupply and declining prices and profit margins. The volatility these markets experience occurs as a result of changes in the supply and demand for products, changes in energy prices and changes in various other economic conditions around the world. This cyclicality and volatility of our industry results in significant fluctuations in profits and cash flow from period to period and over the business cycle.

Natural or other disasters could disrupt our business and result in loss of revenue or in higher expenses.

Any serious disruption at any of our facilities due to hurricane, fire, earthquake, flood, terrorist attack or any other natural or man-made disaster could impair our ability to use our facilities and have a material adverse impact on our revenues and increase our costs and expenses. If there is a natural disaster or other serious disruption at any of these facilities, it could impair our ability to adequately supply our customers and negatively impact our operating results. In addition, many of our current and potential customers are concentrated in specific geographic areas. A disaster in one of these regions could have a material adverse impact on our operations, operating results and financial condition.

While we maintain business recovery plans that are intended to allow us to recover from natural disasters or other events that could disrupt our business, we cannot provide assurances that our plans would fully protect us from all such disasters or events that might result due to climate change. In addition, insurance may not adequately compensate us from any losses incurred as a result of natural or other disasters. Furthermore, in areas prone to frequent natural or other disasters, insurance may become increasingly expensive or not at all available.

Our operations involve risks that may increase our operating costs, which could reduce our profitability.

Although we take precautions to enhance the safety of our operations and minimize the risk of disruptions, our operations are subject to hazards inherent in the manufacturing and marketing of differentiated and commodity chemical products. These hazards include: chemical spills, pipeline leaks

20

and ruptures, storage tank leaks, discharges or releases of toxic or hazardous substances or gases and other hazards incident to the manufacturing, processing, handling, transportation and storage of dangerous chemicals. We are also potentially subject to other hazards, including natural disasters and severe weather; explosions and fires; transportation problems, including interruptions, spills and leaks; mechanical failures; unscheduled downtimes; labor difficulties; remediation complications; and other risks. Many potential hazards can cause bodily injury and loss of life, severe damage to or destruction of property and equipment and environmental damage, and may result in suspension of operations and the imposition of civil or criminal penalties and liabilities. Furthermore, we are subject to present and future claims with respect to workplace exposure, exposure of contractors on our premises as well as other persons located nearby, workers' compensation and other matters.

We maintain property, business interruption and casualty insurance policies which we believe are in accordance with customary industry practices, but we are not fully insured against all potential hazards and risks incident to our business. We maintain property damage and business interruption insurance policies and products liability insurance policies, as well as insurance policies covering other types of risks, including pollution legal liability insurance. Each of these insurance policies is subject to customary exclusions, deductibles and coverage limits, in accordance with industry standards and practices. As a result of market conditions, premiums and deductibles for certain insurance policies can increase substantially and, in some instances, certain insurance may become unavailable or available only for reduced amounts of coverage. If we were to incur a significant liability for which we were not fully insured, it could have a material adverse effect on our business, results of operations, financial condition and liquidity.

In addition, we are subject to various claims and litigation in the ordinary course of business. We are a party to various pending lawsuits and proceedings. For more information, see "Business—Legal Proceedings." It is possible that judgments could be rendered against us in these cases or others in which we could be uninsured or not covered by indemnity and beyond the amounts that we currently have reserved or anticipate incurring for such matters.

We are subject to many environmental and safety regulations that may result in unanticipated costs or liabilities, which could reduce our profitability.

We are subject to extensive federal, state, local and foreign laws, regulations, rules and ordinances relating to pollution, protection of the environment and human health, and the generation, storage, handling, transportation, treatment, disposal and remediation of hazardous substances and waste materials. Actual or alleged violations of environmental laws or permit requirements could result in restrictions or prohibitions on plant operations, substantial civil or criminal sanctions, as well as, under some environmental laws, the assessment of strict liability and/or joint and several liability.

Continually increasing concerns regarding the safety of chemicals in commerce and their potential impact on the environment constitute a growing trend. Governmental, regulatory and societal demands for continuously increasing levels of product safety and environmental protection could result in continued pressure for more stringent regulatory control with respect to the chemical industry. In addition, these concerns could influence public perceptions, the viability of certain products, our reputation, the cost to comply with regulations, and the ability to attract and retain employees. Moreover, changes in environmental regulations could inhibit or interrupt our operations, or require us to modify our facilities or operations. Accordingly, environmental or regulatory matters may cause us to incur significant unanticipated losses, costs or liabilities, which could reduce our profitability.

We could incur significant expenditures in order to comply with existing or future environmental or safety laws. Capital expenditures and costs relating to environmental or safety matters will be subject to evolving regulatory requirements and will depend on the timing of the promulgation and enforcement of specific standards which impose requirements on our operations. Capital expenditures and costs

21

beyond those currently anticipated may therefore be required under existing or future environmental or safety laws.

Furthermore, we may be liable for the costs of investigating and cleaning up environmental contamination on or from our properties or at off-site locations where we disposed of or arranged for the disposal or treatment of hazardous materials or from disposal activities that pre-dated our purchase of our businesses. We may therefore incur additional costs and expenditures beyond those currently anticipated to address all such known and unknown situations under existing and future environmental laws.

Existing or future litigation or legislative initiatives restricting the use of MTBE in gasoline may subject us or our products to environmental liability, materially reduce our sales and/or materially increase our costs.

We produce MTBE, an oxygenate that is blended with gasoline to reduce vehicle air emissions and to enhance the octane rating of gasoline. Litigation or legislative initiatives restricting the use of MTBE in gasoline may subject us or our products to environmental liability or materially adversely affect our sales and costs. Because MTBE has contaminated some water supplies, its use has become controversial in the U.S. and elsewhere, and its use has been effectively eliminated in the U.S. market. We currently market MTBE, either directly or through third parties, to gasoline additive customers located outside the U.S., although there are additional costs associated with such outside-U.S. sales which may result in decreased profitability compared to historical sales in the U.S. We may also elect to use all or a portion of our precursor tertiary butyl alcohol to produce saleable products other than MTBE. If we opt to produce products other than MTBE, necessary modifications to our facilities will require significant capital expenditures and the sale of such other products may produce a lower level of cash flow than that historically produced from the sale of MTBE.

Numerous companies, including refiners, manufacturers and sellers of gasoline, as well as manufacturers of MTBE, have been named as defendants in more than 150 cases in U.S. courts that allege MTBE contamination in groundwater. Many of these cases were settled after the parties engaged in mediation supervised by a court-appointed special settlement master. Beginning in March 2007 and continuing through June 24, 2009, we have been named as a defendant in 18 of these lawsuits pending in New York state and federal courts. For more information, see "Note 19. Commitments and Contingencies—Legal Matters—MTBE Litigation" to the audited consolidated financial statements included elsewhere in this prospectus and "Note 13. Commitments and Contingencies—Legal Matters—MTBE Litigation" to the unaudited condensed consolidated financial statements included elsewhere in this prospectus. The plaintiffs in the MTBE groundwater contamination cases generally seek compensatory damages, punitive damages, injunctive relief, such as monitoring and abatement, and attorney fees. While we currently have insufficient information to meaningfully assess our potential exposure in these cases, we have joined with a larger group of defendants in an effort to mediate the plaintiffs' claims. Mediation in late 2008 and early 2009 was unsuccessful. A further mediation session was held February 3, 2010 which resulted in a tentative settlement in each of the cases in which we have been named. Our allocated portion of the total settlement amount is not material, and we have accrued a liability for the claims equal to our allocated portion of the settlement. It is possible that we could be named as a defendant in additional existing or future MTBE contamination cases. We cannot provide assurances that adverse results against us in existing or future MTBE contamination cases will not have a material adverse effect on our business, results of operations and financial position.

Failure to adequately protect critical data and technology systems could materially affect our operations.

Information technology system failures, network disruptions and breaches of data security could disrupt our operations by causing delays or cancellation of customer orders, impeding the manufacture or shipment of products, processing transactions and reporting financial results, resulting in the unintentional disclosure of customer or our information, or damage to our reputation. While

22

management has taken steps to address these concerns by implementing network security and internal control measures, there can be no assurance that a system failure or data security breach will not have a material adverse effect on our financial condition and operating results.

Our business is dependent on our intellectual property. If our patents are declared invalid or our trade secrets become known to our competitors, our ability to compete may be adversely affected.

Proprietary protection of our processes, apparatuses and other technology is important to our business. Consequently, we may have to rely on judicial enforcement of our patents and other proprietary rights. While a presumption of validity exists with respect to patents issued to us in the U.S., there can be no assurance that any of our patents will not be challenged, invalidated, circumvented or rendered unenforceable. Furthermore, if any pending patent application filed by us does not result in an issued patent, or if patents are issued to us, but such patents do not provide meaningful protection of our intellectual property, then our ability to compete may be adversely affected. Additionally, our competitors or other third parties may obtain patents that restrict or preclude our ability to lawfully produce or sell our products in a competitive manner, which could have a material adverse effect on our business, results of operations, financial condition and liquidity.

We also rely upon unpatented proprietary know-how and continuing technological innovation and other trade secrets to develop and maintain our competitive position. While it is our policy to enter into confidentiality agreements with our employees and third parties to protect our intellectual property, these confidentiality agreements may be breached, may not provide meaningful protection for our trade secrets or proprietary know-how, or adequate remedies may not be available in the event of an unauthorized use or disclosure of our trade secrets and know-how. In addition, others could obtain knowledge of our trade secrets through independent development or other access by legal means. The failure of our patents or confidentiality agreements to protect our processes, apparatuses, technology, trade secrets or proprietary know-how could have a material adverse effect on our business, results of operations, financial condition and liquidity.

Loss of key members of our management could disrupt our business.

We depend on the continued employment and performance of our senior executives and other key members of management. If any of these individuals resigns or becomes unable to continue in his or her present role and is not adequately replaced, our business operations and our ability to implement our growth strategies could be materially disrupted. We generally do not have employment agreements with, and we do not maintain any "key person" life insurance for, any of our executive officers.

Conflicts, military actions, terrorist attacks and general instability throughout the world, and in particular in certain energy-producing nations, along with increased security regulations related to our industry, could adversely affect our business.

Conflicts, military actions and terrorist attacks have precipitated global economic instability and turmoil in world financial markets. Current regional tensions and conflicts in energy-producing nations, including continuing instability in Iran, ongoing military action in Iraq, and other conflicts have caused, and may cause further, increases in raw material costs, particularly natural gas and crude oil based feedstocks, which are used in our operations. The uncertainty surrounding the threat of further armed hostilities, military action or acts of terrorism may impact any or all of our physical facilities and operations, which are located in North America, Europe, Australia, Asia, Africa, South America and the Middle East, or those of our suppliers or customers. Furthermore, the resulting economic disruption caused by such events may result in reduced demand from our customers for our products.

23

A military action or terrorist attack that impacts any of our facilities, or the facilities of our suppliers or customers, could have a material adverse effect on our business. In addition, a number of governments have begun regulatory processes that could lead to new regulations impacting the security of chemical plant locations and the transportation of hazardous chemicals, which could result in higher operating costs. These developments will subject our worldwide operations to increased risks and, depending on their magnitude, could have a material adverse effect on our business, results of operations, financial condition and liquidity.

If our subsidiaries do not make sufficient distributions to us, then we will not be able to make payment on our debts.

Because a significant portion of our operations are conducted by subsidiaries, our cash flow and our ability to service indebtedness, including our ability to pay the interest on our debt when due and principal of such debt at maturity, are dependent to a large extent upon cash dividends and distributions or other transfers from such subsidiaries. Any payment of dividends, distributions, loans or advances by our non-guarantor subsidiaries to us could be subject to restrictions on dividends or repatriation of earnings under applicable local law, monetary transfer restrictions and foreign currency exchange regulations in the jurisdictions in which our subsidiaries operate, and any restrictions imposed by the current and future debt instruments of our subsidiaries. In addition, payments to us by our subsidiaries are contingent upon our subsidiaries' earnings.

Our subsidiaries are separate and distinct legal entities and, except for our guarantor subsidiaries, have no obligation, contingent or otherwise, to pay any amounts due on our debt or to make any funds available for those amounts, whether by dividends, loans, distributions or other payments, and do not guarantee the payment of interest on, or principal of, our debt. Any right that we have to receive any assets of any of our subsidiaries that are not guarantors upon the liquidation or reorganization of any such subsidiary, and the consequent right of holders of notes to realize proceeds from the sale of their assets, will be structurally subordinated to the claims of that subsidiary's creditors, including trade creditors and holders of debt issued by that subsidiary.

Climate change poses both regulatory and physical risks that could adversely impact our results of operations.

In addition to the possible direct economic impact that climate change could have on us, climate change mitigation programs and regulation could significantly increase our costs. Energy costs are a significant component of our overall costs, and climate change regulation may result in significant increases in energy costs. Specifically, our costs could increase if energy companies pass on increased costs to their customers, such as costs resulting from carbon taxes, emission cap and trade programs or renewable portfolio standards. For specific details, see individual risk factors listed above.

Risks Related to the Notes

Despite our current levels of indebtedness, we may incur substantially more debt, which could further increase the risks associated with our substantial indebtedness.